Today, Bloomberg reported that January new home sales dropped substantially, and standing inventory is at an all-time high. Wasn’t it just two weeks ago that we were discussing record new home starts—big numbers not seen in over 33 years?

Hmmm… This news kinda makes you want to sit back and think a little…

Let’s see… January housing starts were 2.276 million (per annum), equating to roughly 190,000 home starts. Today, news reports that January new home sales were down to 1.233 million (per annum), equating to roughly 103,000 home sales. It doesn’t take a rocket scientist (which I’m certainly not) to see that the US housing industry has just added 87,000 excess homes to the market in January 2006. These new homes (once finished) will add to the record number of homes already for sale nationwide (currently 528,000 total).

When you combine the housing information above with (1) The lowest personal savings rate since the Great Depression, (2) Consumer Bankruptcies at an all time high, (3) Increasing interest rate environment, (4) Rising Energy Costs and instability in world oil markets, (5) Continued US Outsourcing and loss of US job market, (6) Failing corporations--GM, Delphi, Ford, US airline industry, etc, (7) Increasing Trade Deficit and US Debt, (8) substantial US dollar problems, (9) Inverted Yield Curve, (10) complete lack of US Government interest in getting our economic house in order, and (11) $1 + Trillion dollars of Interest rate resets in the next 18 months, etc… what do you think will happen to the housing market and our economy? My thoughts: I believe it will be an American Wake Up Call

Anyway, based on the figures released today and the prevailing trend, it’s almost certain the US housing market will continue to cool. If it cools too fast, the abrupt economic fallout could be severe. If it cools slowly, it will be less painful, but any one of the other issues I listed above could create their own potential problems and economic fallout, thus adding to the misery.

Either way, our future doesn’t look nearly as bright as our past, and the housing ATM is going the way of the US government and consumer—completely broke.

This is a very interesting, yet scary time to be alive.

I’ve written other articles about these same issues, and you can read them here, here, here and here.

Monday, February 27, 2006

Sunday, February 26, 2006

The End of Dollar Hegemony

Many returning readers already know my thoughts on the dollar, but for those of you who don’t, I’ll try to quickly summarize: I believe our fiat dollar (the world’s reserve currency) is due for a major correction (devaluation), and when all is said and done, our way of life will completely change.

As the world continues to pay increasingly higher oil prices, cracks in the dollar will begin to appear... Our government officials are spending like mad men while the trade deficit balloons & debt bulges at the seams. Meanwhile, foreign central banks cringe as they see our Federal Reserve printing presses smoking from overuse, and ultimately they begin to realize they'll probably never be repaid.

IMHO, the US dollar’s days, as the world's reserve, is probably very limited. When will we see this happen? Your guess is as good as mine, but I believe it will be sooner (within 15 years) rather than later. With that said, I believe we will experience much economic and geopolitical turmoil before now and the end of this decade, but it will take many, many additional years for the world to transition to a new reserve.

My thoughts for those of you interested in how this relates to the housing bubble: The current US housing bubble is only the latest symptom of broken economic fundamentals and was created by “Easy Al”--through massive liquidity and the lowest interest rates in 40-years. If the dollar happens to collapse before the housing bubble lets out the majority of its excess, the “Bubble” will probably be relegated to a footnote in history, as a dollar collapse will bring the world to its knees. With that said, the roles may be reversed and it may be the housing bubble’s deflation that ultimately brings the demise of the dollar, as 90% of our growth in GDP (2001-05) was due to housing and consumer spending. When the bubble deflates, consumers will lose their "wealth effect" and will have no choice but to pullback on spending. This pullback will send our country into a recession (my prediction is 2007). A U.S. recession will negatively impact the world and we could see a dumping of the dollar (depending on Fed Policy).

Anyway, enough of my “short” summary on the dollar… If you’d like to read more thoughts on the dollar, see my Blog articles here, here, here, and here.

With that behind me, the main reason I’m writing about the dollar today is: Three people independently sent me the same link to one of the finest articles on the US dollar I’ve had the opportunity to read. The article was actually a speech given by Congressman Ron Paul of Texas, before the U.S. House of Representatives on Feb 15, 2006.

If you only read one thing today, I recommend it be this: The End of Dollar Hegemony.

A hundred years ago it was called “dollar diplomacy.” After World War II, and especially after the fall of the Soviet Union in 1989, that policy evolved into “dollar hegemony.” But after all these many years of great success, our dollar dominance is coming to an end.

It has been said, rightly, that he who holds the gold makes the rules. In earlier times it was readily accepted that fair and honest trade required an exchange for something of real value.

First it was simply barter of goods. Then it was discovered that gold held a universal attraction, and was a convenient substitute for more cumbersome barter transactions. Not only did gold facilitate exchange of goods and services, it served as a store of value for those who wanted to save for a rainy day.

Though money developed naturally in the marketplace, as governments grew in power they assumed monopoly control over money. Sometimes governments succeeded in guaranteeing the quality and purity of gold, but in time governments learned to outspend their revenues. New or higher taxes always incurred the disapproval of the people, so it wasn’t long before Kings and Caesars learned how to inflate their currencies by reducing the amount of gold in each coin-- always hoping their subjects wouldn’t discover the fraud. But the people always did, and they strenuously objected.

This helped pressure leaders to seek more gold by conquering other nations. The people became accustomed to living beyond their means, and enjoyed the circuses and bread. Financing extravagances by conquering foreign lands seemed a logical alternative to working harder and producing more. Besides, conquering nations not only brought home gold, they brought home slaves as well. Taxing the people in conquered territories also provided an incentive to build empires. This system of government worked well for a while, but the moral decline of the people led to an unwillingness to produce for themselves. There was a limit to the number of countries that could be sacked for their wealth, and this always brought empires to an end. When gold no longer could be obtained, their military might crumbled. In those days those who held the gold truly wrote the rules and lived well.

That general rule has held fast throughout the ages. When gold was used, and the rules protected honest commerce, productive nations thrived. Whenever wealthy nations-- those with powerful armies and gold-- strived only for empire and easy fortunes to support welfare at home, those nations failed.

Today the principles are the same, but the process is quite different. Gold no longer is the currency of the realm; paper is. The truth now is: “He who prints the money makes the rules”-- at least for the time being. Although gold is not used, the goals are the same: compel foreign countries to produce and subsidize the country with military superiority and control over the monetary printing presses.

Since printing paper money is nothing short of counterfeiting, the issuer of the international currency must always be the country with the military might to guarantee control over the system. This magnificent scheme seems the perfect system for obtaining perpetual wealth for the country that issues the de facto world currency. The one problem, however, is that such a system destroys the character of the counterfeiting nation’s people-- just as was the case when gold was the currency and it was obtained by conquering other nations. And this destroys the incentive to save and produce, while encouraging debt and runaway welfare.

The pressure at home to inflate the currency comes from the corporate welfare recipients, as well as those who demand handouts as compensation for their needs and perceived injuries by others. In both cases personal responsibility for one’s actions is rejected.

When paper money is rejected, or when gold runs out, wealth and political stability are lost. The country then must go from living beyond its means to living beneath its means, until the economic and political systems adjust to the new rules-- rules no longer written by those who ran the now defunct printing press.

“Dollar Diplomacy,” a policy instituted by William Howard Taft and his Secretary of State Philander C. Knox, was designed to enhance U.S. commercial investments in Latin America and the Far East. McKinley concocted a war against Spain in 1898, and (Teddy) Roosevelt’s corollary to the Monroe Doctrine preceded Taft’s aggressive approach to using the U.S. dollar and diplomatic influence to secure U.S. investments abroad. This earned the popular title of “Dollar Diplomacy.” The significance of Roosevelt’s change was that our intervention now could be justified by the mere “appearance” that a country of interest to us was politically or fiscally vulnerable to European control. Not only did we claim a right, but even an official U.S. government “obligation” to protect our commercial interests from Europeans.

This new policy came on the heels of the “gunboat” diplomacy of the late 19th century, and it meant we could buy influence before resorting to the threat of force. By the time the “dollar diplomacy” of William Howard Taft was clearly articulated, the seeds of American empire were planted. And they were destined to grow in the fertile political soil of a country that lost its love and respect for the republic bequeathed to us by the authors of the Constitution. And indeed they did. It wasn’t too long before dollar “diplomacy” became dollar “hegemony” in the second half of the 20th century.

This transition only could have occurred with a dramatic change in monetary policy and the nature of the dollar itself.

Congress created the Federal Reserve System in 1913. Between then and 1971 the principle of sound money was systematically undermined. Between 1913 and 1971, the Federal Reserve found it much easier to expand the money supply at will for financing war or manipulating the economy with little resistance from Congress-- while benefiting the special interests that influence government.

Dollar dominance got a huge boost after World War II. We were spared the destruction that so many other nations suffered, and our coffers were filled with the world’s gold. But the world chose not to return to the discipline of the gold standard, and the politicians applauded. Printing money to pay the bills was a lot more popular than taxing or restraining unnecessary spending. In spite of the short-term benefits, imbalances were institutionalized for decades to come.

The 1944 Bretton Woods agreement solidified the dollar as the preeminent world reserve currency, replacing the British pound. Due to our political and military muscle, and because we had a huge amount of physical gold, the world readily accepted our dollar (defined as 1/35th of an ounce of gold) as the world’s reserve currency. The dollar was said to be “as good as gold,” and convertible to all foreign central banks at that rate. For American citizens, however, it remained illegal to own. This was a gold-exchange standard that from inception was doomed to fail.

The U.S. did exactly what many predicted she would do. She printed more dollars for which there was no gold backing. But the world was content to accept those dollars for more than 25 years with little question-- until the French and others in the late 1960s demanded we fulfill our promise to pay one ounce of gold for each $35 they delivered to the U.S. Treasury. This resulted in a huge gold drain that brought an end to a very poorly devised pseudo-gold standard.

It all ended on August 15, 1971, when Nixon closed the gold window and refused to pay out any of our remaining 280 million ounces of gold. In essence, we declared our insolvency and everyone recognized some other monetary system had to be devised in order to bring stability to the markets.

Amazingly, a new system was devised which allowed the U.S. to operate the printing presses for the world reserve currency with no restraints placed on it-- not even a pretense of gold convertibility, none whatsoever! Though the new policy was even more deeply flawed, it nevertheless opened the door for dollar hegemony to spread.

Realizing the world was embarking on something new and mind boggling, elite money managers, with especially strong support from U.S. authorities, struck an agreement with OPEC to price oil in U.S. dollars exclusively for all worldwide transactions. This gave the dollar a special place among world currencies and in essence “backed” the dollar with oil. In return, the U.S. promised to protect the various oil-rich kingdoms in the Persian Gulf against threat of invasion or domestic coup. This arrangement helped ignite the radical Islamic movement among those who resented our influence in the region. The arrangement gave the dollar artificial strength, with tremendous financial benefits for the United States. It allowed us to export our monetary inflation by buying oil and other goods at a great discount as dollar influence flourished.

This post-Bretton Woods system was much more fragile than the system that existed between 1945 and 1971. Though the dollar/oil arrangement was helpful, it was not nearly as stable as the pseudo gold standard under Bretton Woods. It certainly was less stable than the gold standard of the late 19th century.

During the 1970s the dollar nearly collapsed, as oil prices surged and gold skyrocketed to $800 an ounce. By 1979 interest rates of 21% were required to rescue the system. The pressure on the dollar in the 1970s, in spite of the benefits accrued to it, reflected reckless budget deficits and monetary inflation during the 1960s. The markets were not fooled by LBJ’s claim that we could afford both “guns and butter.”

Once again the dollar was rescued, and this ushered in the age of true dollar hegemony lasting from the early 1980s to the present. With tremendous cooperation coming from the central banks and international commercial banks, the dollar was accepted as if it were gold.

Fed Chair Alan Greenspan, on several occasions before the House Banking Committee, answered my challenges to him about his previously held favorable views on gold by claiming that he and other central bankers had gotten paper money-- i.e. the dollar system-- to respond as if it were gold. Each time I strongly disagreed, and pointed out that if they had achieved such a feat they would have defied centuries of economic history regarding the need for money to be something of real value. He smugly and confidently concurred with this.

In recent years central banks and various financial institutions, all with vested interests in maintaining a workable fiat dollar standard, were not secretive about selling and loaning large amounts of gold to the market even while decreasing gold prices raised serious questions about the wisdom of such a policy. They never admitted to gold price fixing, but the evidence is abundant that they believed if the gold price fell it would convey a sense of confidence to the market, confidence that they indeed had achieved amazing success in turning paper into gold.

Increasing gold prices historically are viewed as an indicator of distrust in paper currency. This recent effort was not a whole lot different than the U.S. Treasury selling gold at $35 an ounce in the 1960s, in an attempt to convince the world the dollar was sound and as good as gold. Even during the Depression, one of Roosevelt’s first acts was to remove free market gold pricing as an indication of a flawed monetary system by making it illegal for American citizens to own gold. Economic law eventually limited that effort, as it did in the early 1970s when our Treasury and the IMF tried to fix the price of gold by dumping tons into the market to dampen the enthusiasm of those seeking a safe haven for a falling dollar after gold ownership was re-legalized.

Once again the effort between 1980 and 2000 to fool the market as to the true value of the dollar proved unsuccessful. In the past 5 years the dollar has been devalued in terms of gold by more than 50%. You just can’t fool all the people all the time, even with the power of the mighty printing press and money creating system of the Federal Reserve.

Even with all the shortcomings of the fiat monetary system, dollar influence thrived. The results seemed beneficial, but gross distortions built into the system remained. And true to form, Washington politicians are only too anxious to solve the problems cropping up with window dressing, while failing to understand and deal with the underlying flawed policy. Protectionism, fixing exchange rates, punitive tariffs, politically motivated sanctions, corporate subsidies, international trade management, price controls, interest rate and wage controls, super-nationalist sentiments, threats of force, and even war are resorted to—all to solve the problems artificially created by deeply flawed monetary and economic systems.

In the short run, the issuer of a fiat reserve currency can accrue great economic benefits. In the long run, it poses a threat to the country issuing the world currency. In this case that’s the United States. As long as foreign countries take our dollars in return for real goods, we come out ahead. This is a benefit many in Congress fail to recognize, as they bash China for maintaining a positive trade balance with us. But this leads to a loss of manufacturing jobs to overseas markets, as we become more dependent on others and less self-sufficient. Foreign countries accumulate our dollars due to their high savings rates, and graciously loan them back to us at low interest rates to finance our excessive consumption.

It sounds like a great deal for everyone, except the time will come when our dollars-- due to their depreciation-- will be received less enthusiastically or even be rejected by foreign countries. That could create a whole new ballgame and force us to pay a price for living beyond our means and our production. The shift in sentiment regarding the dollar has already started, but the worst is yet to come.

The agreement with OPEC in the 1970s to price oil in dollars has provided tremendous artificial strength to the dollar as the preeminent reserve currency. This has created a universal demand for the dollar, and soaks up the huge number of new dollars generated each year. Last year alone M3 increased over $700 billion.

The artificial demand for our dollar, along with our military might, places us in the unique position to “rule” the world without productive work or savings, and without limits on consumer spending or deficits. The problem is, it can’t last.

Price inflation is raising its ugly head, and the NASDAQ bubble-- generated by easy money-- has burst. The housing bubble likewise created is deflating. Gold prices have doubled, and federal spending is out of sight with zero political will to rein it in. The trade deficit last year was over $728 billion. A $2 trillion war is raging, and plans are being laid to expand the war into Iran and possibly Syria. The only restraining force will be the world’s rejection of the dollar. It’s bound to come and create conditions worse than 1979-1980, which required 21% interest rates to correct. But everything possible will be done to protect the dollar in the meantime. We have a shared interest with those who hold our dollars to keep the whole charade going.

Greenspan, in his first speech after leaving the Fed, said that gold prices were up because of concern about terrorism, and not because of monetary concerns or because he created too many dollars during his tenure. Gold has to be discredited and the dollar propped up. Even when the dollar comes under serious attack by market forces, the central banks and the IMF surely will do everything conceivable to soak up the dollars in hope of restoring stability. Eventually they will fail.

Most importantly, the dollar/oil relationship has to be maintained to keep the dollar as a preeminent currency. Any attack on this relationship will be forcefully challenged—as it already has been.

In November 2000 Saddam Hussein demanded Euros for his oil. His arrogance was a threat to the dollar; his lack of any military might was never a threat. At the first cabinet meeting with the new administration in 2001, as reported by Treasury Secretary Paul O’Neill, the major topic was how we would get rid of Saddam Hussein-- though there was no evidence whatsoever he posed a threat to us. This deep concern for Saddam Hussein surprised and shocked O’Neill.

It now is common knowledge that the immediate reaction of the administration after 9/11 revolved around how they could connect Saddam Hussein to the attacks, to justify an invasion and overthrow of his government. Even with no evidence of any connection to 9/11, or evidence of weapons of mass destruction, public and congressional support was generated through distortions and flat out misrepresentation of the facts to justify overthrowing Saddam Hussein.

There was no public talk of removing Saddam Hussein because of his attack on the integrity of the dollar as a reserve currency by selling oil in Euros. Many believe this was the real reason for our obsession with Iraq. I doubt it was the only reason, but it may well have played a significant role in our motivation to wage war. Within a very short period after the military victory, all Iraqi oil sales were carried out in dollars. The Euro was abandoned.

In 2001, Venezuela’s ambassador to Russia spoke of Venezuela switching to the Euro for all their oil sales. Within a year there was a coup attempt against Chavez, reportedly with assistance from our CIA.

After these attempts to nudge the Euro toward replacing the dollar as the world’s reserve currency were met with resistance, the sharp fall of the dollar against the Euro was reversed. These events may well have played a significant role in maintaining dollar dominance.

It’s become clear the U.S. administration was sympathetic to those who plotted the overthrow of Chavez, and was embarrassed by its failure. The fact that Chavez was democratically elected had little influence on which side we supported.

Now, a new attempt is being made against the petrodollar system. Iran, another member of the “axis of evil,” has announced her plans to initiate an oil bourse in March of this year. Guess what, the oil sales will be priced Euros, not dollars.

Most Americans forget how our policies have systematically and needlessly antagonized the Iranians over the years. In 1953 the CIA helped overthrow a democratically elected president, Mohammed Mossadeqh, and install the authoritarian Shah, who was friendly to the U.S. The Iranians were still fuming over this when the hostages were seized in 1979. Our alliance with Saddam Hussein in his invasion of Iran in the early 1980s did not help matters, and obviously did not do much for our relationship with Saddam Hussein. The administration announcement in 2001 that Iran was part of the axis of evil didn’t do much to improve the diplomatic relationship between our two countries. Recent threats over nuclear power, while ignoring the fact that they are surrounded by countries with nuclear weapons, doesn’t seem to register with those who continue to provoke Iran. With what most Muslims perceive as our war against Islam, and this recent history, there’s little wonder why Iran might choose to harm America by undermining the dollar. Iran, like Iraq, has zero capability to attack us. But that didn’t stop us from turning Saddam Hussein into a modern day Hitler ready to take over the world. Now Iran, especially since she’s made plans for pricing oil in Euros, has been on the receiving end of a propaganda war not unlike that waged against Iraq before our invasion.

It’s not likely that maintaining dollar supremacy was the only motivating factor for the war against Iraq, nor for agitating against Iran. Though the real reasons for going to war are complex, we now know the reasons given before the war started, like the presence of weapons of mass destruction and Saddam Hussein’s connection to 9/11, were false. The dollar’s importance is obvious, but this does not diminish the influence of the distinct plans laid out years ago by the neo-conservatives to remake the Middle East. Israel’s influence, as well as that of the Christian Zionists, likewise played a role in prosecuting this war. Protecting “our” oil supplies has influenced our Middle East policy for decades.

But the truth is that paying the bills for this aggressive intervention is impossible the old fashioned way, with more taxes, more savings, and more production by the American people. Much of the expense of the Persian Gulf War in 1991 was shouldered by many of our willing allies. That’s not so today. Now, more than ever, the dollar hegemony-- it’s dominance as the world reserve currency-- is required to finance our huge war expenditures. This $2 trillion never-ending war must be paid for, one way or another. Dollar hegemony provides the vehicle to do just that.

For the most part the true victims aren’t aware of how they pay the bills. The license to create money out of thin air allows the bills to be paid through price inflation. American citizens, as well as average citizens of Japan, China, and other countries suffer from price inflation, which represents the “tax” that pays the bills for our military adventures. That is until the fraud is discovered, and the foreign producers decide not to take dollars nor hold them very long in payment for their goods. Everything possible is done to prevent the fraud of the monetary system from being exposed to the masses who suffer from it. If oil markets replace dollars with Euros, it would in time curtail our ability to continue to print, without restraint, the world’s reserve currency.

It is an unbelievable benefit to us to import valuable goods and export depreciating dollars. The exporting countries have become addicted to our purchases for their economic growth. This dependency makes them allies in continuing the fraud, and their participation keeps the dollar’s value artificially high. If this system were workable long term, American citizens would never have to work again. We too could enjoy “bread and circuses” just as the Romans did, but their gold finally ran out and the inability of Rome to continue to plunder conquered nations brought an end to her empire.

The same thing will happen to us if we don’t change our ways. Though we don’t occupy foreign countries to directly plunder, we nevertheless have spread our troops across 130 nations of the world. Our intense effort to spread our power in the oil-rich Middle East is not a coincidence. But unlike the old days, we don’t declare direct ownership of the natural resources-- we just insist that we can buy what we want and pay for it with our paper money. Any country that challenges our authority does so at great risk.

Once again Congress has bought into the war propaganda against Iran, just as it did against Iraq. Arguments are now made for attacking Iran economically, and militarily if necessary. These arguments are all based on the same false reasons given for the ill-fated and costly occupation of Iraq.

Our whole economic system depends on continuing the current monetary arrangement, which means recycling the dollar is crucial. Currently, we borrow over $700 billion every year from our gracious benefactors, who work hard and take our paper for their goods. Then we borrow all the money we need to secure the empire (DOD budget $450 billion) plus more. The military might we enjoy becomes the “backing” of our currency. There are no other countries that can challenge our military superiority, and therefore they have little choice but to accept the dollars we declare are today’s “gold.” This is why countries that challenge the system-- like Iraq, Iran and Venezuela-- become targets of our plans for regime change.

Ironically, dollar superiority depends on our strong military, and our strong military depends on the dollar. As long as foreign recipients take our dollars for real goods and are willing to finance our extravagant consumption and militarism, the status quo will continue regardless of how huge our foreign debt and current account deficit become.

But real threats come from our political adversaries who are incapable of confronting us militarily, yet are not bashful about confronting us economically. That’s why we see the new challenge from Iran being taken so seriously. The urgent arguments about Iran posing a military threat to the security of the United States are no more plausible than the false charges levied against Iraq. Yet there is no effort to resist this march to confrontation by those who grandstand for political reasons against the Iraq war.It seems that the people and Congress are easily persuaded by the jingoism of the preemptive war promoters. It’s only after the cost in human life and dollars are tallied up that the people object to unwise militarism.

The strange thing is that the failure in Iraq is now apparent to a large majority of American people, yet they and Congress are acquiescing to the call for a needless and dangerous confrontation with Iran.

But then again, our failure to find Osama bin Laden and destroy his network did not dissuade us from taking on the Iraqis in a war totally unrelated to 9/11.

Concern for pricing oil only in dollars helps explain our willingness to drop everything and teach Saddam Hussein a lesson for his defiance in demanding Euros for oil.

And once again there’s this urgent call for sanctions and threats of force against Iran at the precise time Iran is opening a new oil exchange with all transactions in Euros.

Using force to compel people to accept money without real value can only work in the short run. It ultimately leads to economic dislocation, both domestic and international, and always ends with a price to be paid.

The economic law that honest exchange demands only things of real value as currency cannot be repealed. The chaos that one day will ensue from our 35-year experiment with worldwide fiat money will require a return to money of real value. We will know that day is approaching when oil-producing countries demand gold, or its equivalent, for their oil rather than dollars or Euros. The sooner the better.

As the world continues to pay increasingly higher oil prices, cracks in the dollar will begin to appear... Our government officials are spending like mad men while the trade deficit balloons & debt bulges at the seams. Meanwhile, foreign central banks cringe as they see our Federal Reserve printing presses smoking from overuse, and ultimately they begin to realize they'll probably never be repaid.

IMHO, the US dollar’s days, as the world's reserve, is probably very limited. When will we see this happen? Your guess is as good as mine, but I believe it will be sooner (within 15 years) rather than later. With that said, I believe we will experience much economic and geopolitical turmoil before now and the end of this decade, but it will take many, many additional years for the world to transition to a new reserve.

My thoughts for those of you interested in how this relates to the housing bubble: The current US housing bubble is only the latest symptom of broken economic fundamentals and was created by “Easy Al”--through massive liquidity and the lowest interest rates in 40-years. If the dollar happens to collapse before the housing bubble lets out the majority of its excess, the “Bubble” will probably be relegated to a footnote in history, as a dollar collapse will bring the world to its knees. With that said, the roles may be reversed and it may be the housing bubble’s deflation that ultimately brings the demise of the dollar, as 90% of our growth in GDP (2001-05) was due to housing and consumer spending. When the bubble deflates, consumers will lose their "wealth effect" and will have no choice but to pullback on spending. This pullback will send our country into a recession (my prediction is 2007). A U.S. recession will negatively impact the world and we could see a dumping of the dollar (depending on Fed Policy).

Anyway, enough of my “short” summary on the dollar… If you’d like to read more thoughts on the dollar, see my Blog articles here, here, here, and here.

With that behind me, the main reason I’m writing about the dollar today is: Three people independently sent me the same link to one of the finest articles on the US dollar I’ve had the opportunity to read. The article was actually a speech given by Congressman Ron Paul of Texas, before the U.S. House of Representatives on Feb 15, 2006.

If you only read one thing today, I recommend it be this: The End of Dollar Hegemony.

A hundred years ago it was called “dollar diplomacy.” After World War II, and especially after the fall of the Soviet Union in 1989, that policy evolved into “dollar hegemony.” But after all these many years of great success, our dollar dominance is coming to an end.

It has been said, rightly, that he who holds the gold makes the rules. In earlier times it was readily accepted that fair and honest trade required an exchange for something of real value.

First it was simply barter of goods. Then it was discovered that gold held a universal attraction, and was a convenient substitute for more cumbersome barter transactions. Not only did gold facilitate exchange of goods and services, it served as a store of value for those who wanted to save for a rainy day.

Though money developed naturally in the marketplace, as governments grew in power they assumed monopoly control over money. Sometimes governments succeeded in guaranteeing the quality and purity of gold, but in time governments learned to outspend their revenues. New or higher taxes always incurred the disapproval of the people, so it wasn’t long before Kings and Caesars learned how to inflate their currencies by reducing the amount of gold in each coin-- always hoping their subjects wouldn’t discover the fraud. But the people always did, and they strenuously objected.

This helped pressure leaders to seek more gold by conquering other nations. The people became accustomed to living beyond their means, and enjoyed the circuses and bread. Financing extravagances by conquering foreign lands seemed a logical alternative to working harder and producing more. Besides, conquering nations not only brought home gold, they brought home slaves as well. Taxing the people in conquered territories also provided an incentive to build empires. This system of government worked well for a while, but the moral decline of the people led to an unwillingness to produce for themselves. There was a limit to the number of countries that could be sacked for their wealth, and this always brought empires to an end. When gold no longer could be obtained, their military might crumbled. In those days those who held the gold truly wrote the rules and lived well.

That general rule has held fast throughout the ages. When gold was used, and the rules protected honest commerce, productive nations thrived. Whenever wealthy nations-- those with powerful armies and gold-- strived only for empire and easy fortunes to support welfare at home, those nations failed.

Today the principles are the same, but the process is quite different. Gold no longer is the currency of the realm; paper is. The truth now is: “He who prints the money makes the rules”-- at least for the time being. Although gold is not used, the goals are the same: compel foreign countries to produce and subsidize the country with military superiority and control over the monetary printing presses.

Since printing paper money is nothing short of counterfeiting, the issuer of the international currency must always be the country with the military might to guarantee control over the system. This magnificent scheme seems the perfect system for obtaining perpetual wealth for the country that issues the de facto world currency. The one problem, however, is that such a system destroys the character of the counterfeiting nation’s people-- just as was the case when gold was the currency and it was obtained by conquering other nations. And this destroys the incentive to save and produce, while encouraging debt and runaway welfare.

The pressure at home to inflate the currency comes from the corporate welfare recipients, as well as those who demand handouts as compensation for their needs and perceived injuries by others. In both cases personal responsibility for one’s actions is rejected.

When paper money is rejected, or when gold runs out, wealth and political stability are lost. The country then must go from living beyond its means to living beneath its means, until the economic and political systems adjust to the new rules-- rules no longer written by those who ran the now defunct printing press.

“Dollar Diplomacy,” a policy instituted by William Howard Taft and his Secretary of State Philander C. Knox, was designed to enhance U.S. commercial investments in Latin America and the Far East. McKinley concocted a war against Spain in 1898, and (Teddy) Roosevelt’s corollary to the Monroe Doctrine preceded Taft’s aggressive approach to using the U.S. dollar and diplomatic influence to secure U.S. investments abroad. This earned the popular title of “Dollar Diplomacy.” The significance of Roosevelt’s change was that our intervention now could be justified by the mere “appearance” that a country of interest to us was politically or fiscally vulnerable to European control. Not only did we claim a right, but even an official U.S. government “obligation” to protect our commercial interests from Europeans.

This new policy came on the heels of the “gunboat” diplomacy of the late 19th century, and it meant we could buy influence before resorting to the threat of force. By the time the “dollar diplomacy” of William Howard Taft was clearly articulated, the seeds of American empire were planted. And they were destined to grow in the fertile political soil of a country that lost its love and respect for the republic bequeathed to us by the authors of the Constitution. And indeed they did. It wasn’t too long before dollar “diplomacy” became dollar “hegemony” in the second half of the 20th century.

This transition only could have occurred with a dramatic change in monetary policy and the nature of the dollar itself.

Congress created the Federal Reserve System in 1913. Between then and 1971 the principle of sound money was systematically undermined. Between 1913 and 1971, the Federal Reserve found it much easier to expand the money supply at will for financing war or manipulating the economy with little resistance from Congress-- while benefiting the special interests that influence government.

Dollar dominance got a huge boost after World War II. We were spared the destruction that so many other nations suffered, and our coffers were filled with the world’s gold. But the world chose not to return to the discipline of the gold standard, and the politicians applauded. Printing money to pay the bills was a lot more popular than taxing or restraining unnecessary spending. In spite of the short-term benefits, imbalances were institutionalized for decades to come.

The 1944 Bretton Woods agreement solidified the dollar as the preeminent world reserve currency, replacing the British pound. Due to our political and military muscle, and because we had a huge amount of physical gold, the world readily accepted our dollar (defined as 1/35th of an ounce of gold) as the world’s reserve currency. The dollar was said to be “as good as gold,” and convertible to all foreign central banks at that rate. For American citizens, however, it remained illegal to own. This was a gold-exchange standard that from inception was doomed to fail.

The U.S. did exactly what many predicted she would do. She printed more dollars for which there was no gold backing. But the world was content to accept those dollars for more than 25 years with little question-- until the French and others in the late 1960s demanded we fulfill our promise to pay one ounce of gold for each $35 they delivered to the U.S. Treasury. This resulted in a huge gold drain that brought an end to a very poorly devised pseudo-gold standard.

It all ended on August 15, 1971, when Nixon closed the gold window and refused to pay out any of our remaining 280 million ounces of gold. In essence, we declared our insolvency and everyone recognized some other monetary system had to be devised in order to bring stability to the markets.

Amazingly, a new system was devised which allowed the U.S. to operate the printing presses for the world reserve currency with no restraints placed on it-- not even a pretense of gold convertibility, none whatsoever! Though the new policy was even more deeply flawed, it nevertheless opened the door for dollar hegemony to spread.

Realizing the world was embarking on something new and mind boggling, elite money managers, with especially strong support from U.S. authorities, struck an agreement with OPEC to price oil in U.S. dollars exclusively for all worldwide transactions. This gave the dollar a special place among world currencies and in essence “backed” the dollar with oil. In return, the U.S. promised to protect the various oil-rich kingdoms in the Persian Gulf against threat of invasion or domestic coup. This arrangement helped ignite the radical Islamic movement among those who resented our influence in the region. The arrangement gave the dollar artificial strength, with tremendous financial benefits for the United States. It allowed us to export our monetary inflation by buying oil and other goods at a great discount as dollar influence flourished.

This post-Bretton Woods system was much more fragile than the system that existed between 1945 and 1971. Though the dollar/oil arrangement was helpful, it was not nearly as stable as the pseudo gold standard under Bretton Woods. It certainly was less stable than the gold standard of the late 19th century.

During the 1970s the dollar nearly collapsed, as oil prices surged and gold skyrocketed to $800 an ounce. By 1979 interest rates of 21% were required to rescue the system. The pressure on the dollar in the 1970s, in spite of the benefits accrued to it, reflected reckless budget deficits and monetary inflation during the 1960s. The markets were not fooled by LBJ’s claim that we could afford both “guns and butter.”

Once again the dollar was rescued, and this ushered in the age of true dollar hegemony lasting from the early 1980s to the present. With tremendous cooperation coming from the central banks and international commercial banks, the dollar was accepted as if it were gold.

Fed Chair Alan Greenspan, on several occasions before the House Banking Committee, answered my challenges to him about his previously held favorable views on gold by claiming that he and other central bankers had gotten paper money-- i.e. the dollar system-- to respond as if it were gold. Each time I strongly disagreed, and pointed out that if they had achieved such a feat they would have defied centuries of economic history regarding the need for money to be something of real value. He smugly and confidently concurred with this.

In recent years central banks and various financial institutions, all with vested interests in maintaining a workable fiat dollar standard, were not secretive about selling and loaning large amounts of gold to the market even while decreasing gold prices raised serious questions about the wisdom of such a policy. They never admitted to gold price fixing, but the evidence is abundant that they believed if the gold price fell it would convey a sense of confidence to the market, confidence that they indeed had achieved amazing success in turning paper into gold.

Increasing gold prices historically are viewed as an indicator of distrust in paper currency. This recent effort was not a whole lot different than the U.S. Treasury selling gold at $35 an ounce in the 1960s, in an attempt to convince the world the dollar was sound and as good as gold. Even during the Depression, one of Roosevelt’s first acts was to remove free market gold pricing as an indication of a flawed monetary system by making it illegal for American citizens to own gold. Economic law eventually limited that effort, as it did in the early 1970s when our Treasury and the IMF tried to fix the price of gold by dumping tons into the market to dampen the enthusiasm of those seeking a safe haven for a falling dollar after gold ownership was re-legalized.

Once again the effort between 1980 and 2000 to fool the market as to the true value of the dollar proved unsuccessful. In the past 5 years the dollar has been devalued in terms of gold by more than 50%. You just can’t fool all the people all the time, even with the power of the mighty printing press and money creating system of the Federal Reserve.

Even with all the shortcomings of the fiat monetary system, dollar influence thrived. The results seemed beneficial, but gross distortions built into the system remained. And true to form, Washington politicians are only too anxious to solve the problems cropping up with window dressing, while failing to understand and deal with the underlying flawed policy. Protectionism, fixing exchange rates, punitive tariffs, politically motivated sanctions, corporate subsidies, international trade management, price controls, interest rate and wage controls, super-nationalist sentiments, threats of force, and even war are resorted to—all to solve the problems artificially created by deeply flawed monetary and economic systems.

In the short run, the issuer of a fiat reserve currency can accrue great economic benefits. In the long run, it poses a threat to the country issuing the world currency. In this case that’s the United States. As long as foreign countries take our dollars in return for real goods, we come out ahead. This is a benefit many in Congress fail to recognize, as they bash China for maintaining a positive trade balance with us. But this leads to a loss of manufacturing jobs to overseas markets, as we become more dependent on others and less self-sufficient. Foreign countries accumulate our dollars due to their high savings rates, and graciously loan them back to us at low interest rates to finance our excessive consumption.

It sounds like a great deal for everyone, except the time will come when our dollars-- due to their depreciation-- will be received less enthusiastically or even be rejected by foreign countries. That could create a whole new ballgame and force us to pay a price for living beyond our means and our production. The shift in sentiment regarding the dollar has already started, but the worst is yet to come.

The agreement with OPEC in the 1970s to price oil in dollars has provided tremendous artificial strength to the dollar as the preeminent reserve currency. This has created a universal demand for the dollar, and soaks up the huge number of new dollars generated each year. Last year alone M3 increased over $700 billion.

The artificial demand for our dollar, along with our military might, places us in the unique position to “rule” the world without productive work or savings, and without limits on consumer spending or deficits. The problem is, it can’t last.

Price inflation is raising its ugly head, and the NASDAQ bubble-- generated by easy money-- has burst. The housing bubble likewise created is deflating. Gold prices have doubled, and federal spending is out of sight with zero political will to rein it in. The trade deficit last year was over $728 billion. A $2 trillion war is raging, and plans are being laid to expand the war into Iran and possibly Syria. The only restraining force will be the world’s rejection of the dollar. It’s bound to come and create conditions worse than 1979-1980, which required 21% interest rates to correct. But everything possible will be done to protect the dollar in the meantime. We have a shared interest with those who hold our dollars to keep the whole charade going.

Greenspan, in his first speech after leaving the Fed, said that gold prices were up because of concern about terrorism, and not because of monetary concerns or because he created too many dollars during his tenure. Gold has to be discredited and the dollar propped up. Even when the dollar comes under serious attack by market forces, the central banks and the IMF surely will do everything conceivable to soak up the dollars in hope of restoring stability. Eventually they will fail.

Most importantly, the dollar/oil relationship has to be maintained to keep the dollar as a preeminent currency. Any attack on this relationship will be forcefully challenged—as it already has been.

In November 2000 Saddam Hussein demanded Euros for his oil. His arrogance was a threat to the dollar; his lack of any military might was never a threat. At the first cabinet meeting with the new administration in 2001, as reported by Treasury Secretary Paul O’Neill, the major topic was how we would get rid of Saddam Hussein-- though there was no evidence whatsoever he posed a threat to us. This deep concern for Saddam Hussein surprised and shocked O’Neill.

It now is common knowledge that the immediate reaction of the administration after 9/11 revolved around how they could connect Saddam Hussein to the attacks, to justify an invasion and overthrow of his government. Even with no evidence of any connection to 9/11, or evidence of weapons of mass destruction, public and congressional support was generated through distortions and flat out misrepresentation of the facts to justify overthrowing Saddam Hussein.

There was no public talk of removing Saddam Hussein because of his attack on the integrity of the dollar as a reserve currency by selling oil in Euros. Many believe this was the real reason for our obsession with Iraq. I doubt it was the only reason, but it may well have played a significant role in our motivation to wage war. Within a very short period after the military victory, all Iraqi oil sales were carried out in dollars. The Euro was abandoned.

In 2001, Venezuela’s ambassador to Russia spoke of Venezuela switching to the Euro for all their oil sales. Within a year there was a coup attempt against Chavez, reportedly with assistance from our CIA.

After these attempts to nudge the Euro toward replacing the dollar as the world’s reserve currency were met with resistance, the sharp fall of the dollar against the Euro was reversed. These events may well have played a significant role in maintaining dollar dominance.

It’s become clear the U.S. administration was sympathetic to those who plotted the overthrow of Chavez, and was embarrassed by its failure. The fact that Chavez was democratically elected had little influence on which side we supported.

Now, a new attempt is being made against the petrodollar system. Iran, another member of the “axis of evil,” has announced her plans to initiate an oil bourse in March of this year. Guess what, the oil sales will be priced Euros, not dollars.

Most Americans forget how our policies have systematically and needlessly antagonized the Iranians over the years. In 1953 the CIA helped overthrow a democratically elected president, Mohammed Mossadeqh, and install the authoritarian Shah, who was friendly to the U.S. The Iranians were still fuming over this when the hostages were seized in 1979. Our alliance with Saddam Hussein in his invasion of Iran in the early 1980s did not help matters, and obviously did not do much for our relationship with Saddam Hussein. The administration announcement in 2001 that Iran was part of the axis of evil didn’t do much to improve the diplomatic relationship between our two countries. Recent threats over nuclear power, while ignoring the fact that they are surrounded by countries with nuclear weapons, doesn’t seem to register with those who continue to provoke Iran. With what most Muslims perceive as our war against Islam, and this recent history, there’s little wonder why Iran might choose to harm America by undermining the dollar. Iran, like Iraq, has zero capability to attack us. But that didn’t stop us from turning Saddam Hussein into a modern day Hitler ready to take over the world. Now Iran, especially since she’s made plans for pricing oil in Euros, has been on the receiving end of a propaganda war not unlike that waged against Iraq before our invasion.

It’s not likely that maintaining dollar supremacy was the only motivating factor for the war against Iraq, nor for agitating against Iran. Though the real reasons for going to war are complex, we now know the reasons given before the war started, like the presence of weapons of mass destruction and Saddam Hussein’s connection to 9/11, were false. The dollar’s importance is obvious, but this does not diminish the influence of the distinct plans laid out years ago by the neo-conservatives to remake the Middle East. Israel’s influence, as well as that of the Christian Zionists, likewise played a role in prosecuting this war. Protecting “our” oil supplies has influenced our Middle East policy for decades.

But the truth is that paying the bills for this aggressive intervention is impossible the old fashioned way, with more taxes, more savings, and more production by the American people. Much of the expense of the Persian Gulf War in 1991 was shouldered by many of our willing allies. That’s not so today. Now, more than ever, the dollar hegemony-- it’s dominance as the world reserve currency-- is required to finance our huge war expenditures. This $2 trillion never-ending war must be paid for, one way or another. Dollar hegemony provides the vehicle to do just that.

For the most part the true victims aren’t aware of how they pay the bills. The license to create money out of thin air allows the bills to be paid through price inflation. American citizens, as well as average citizens of Japan, China, and other countries suffer from price inflation, which represents the “tax” that pays the bills for our military adventures. That is until the fraud is discovered, and the foreign producers decide not to take dollars nor hold them very long in payment for their goods. Everything possible is done to prevent the fraud of the monetary system from being exposed to the masses who suffer from it. If oil markets replace dollars with Euros, it would in time curtail our ability to continue to print, without restraint, the world’s reserve currency.

It is an unbelievable benefit to us to import valuable goods and export depreciating dollars. The exporting countries have become addicted to our purchases for their economic growth. This dependency makes them allies in continuing the fraud, and their participation keeps the dollar’s value artificially high. If this system were workable long term, American citizens would never have to work again. We too could enjoy “bread and circuses” just as the Romans did, but their gold finally ran out and the inability of Rome to continue to plunder conquered nations brought an end to her empire.

The same thing will happen to us if we don’t change our ways. Though we don’t occupy foreign countries to directly plunder, we nevertheless have spread our troops across 130 nations of the world. Our intense effort to spread our power in the oil-rich Middle East is not a coincidence. But unlike the old days, we don’t declare direct ownership of the natural resources-- we just insist that we can buy what we want and pay for it with our paper money. Any country that challenges our authority does so at great risk.

Once again Congress has bought into the war propaganda against Iran, just as it did against Iraq. Arguments are now made for attacking Iran economically, and militarily if necessary. These arguments are all based on the same false reasons given for the ill-fated and costly occupation of Iraq.

Our whole economic system depends on continuing the current monetary arrangement, which means recycling the dollar is crucial. Currently, we borrow over $700 billion every year from our gracious benefactors, who work hard and take our paper for their goods. Then we borrow all the money we need to secure the empire (DOD budget $450 billion) plus more. The military might we enjoy becomes the “backing” of our currency. There are no other countries that can challenge our military superiority, and therefore they have little choice but to accept the dollars we declare are today’s “gold.” This is why countries that challenge the system-- like Iraq, Iran and Venezuela-- become targets of our plans for regime change.

Ironically, dollar superiority depends on our strong military, and our strong military depends on the dollar. As long as foreign recipients take our dollars for real goods and are willing to finance our extravagant consumption and militarism, the status quo will continue regardless of how huge our foreign debt and current account deficit become.

But real threats come from our political adversaries who are incapable of confronting us militarily, yet are not bashful about confronting us economically. That’s why we see the new challenge from Iran being taken so seriously. The urgent arguments about Iran posing a military threat to the security of the United States are no more plausible than the false charges levied against Iraq. Yet there is no effort to resist this march to confrontation by those who grandstand for political reasons against the Iraq war.It seems that the people and Congress are easily persuaded by the jingoism of the preemptive war promoters. It’s only after the cost in human life and dollars are tallied up that the people object to unwise militarism.

The strange thing is that the failure in Iraq is now apparent to a large majority of American people, yet they and Congress are acquiescing to the call for a needless and dangerous confrontation with Iran.

But then again, our failure to find Osama bin Laden and destroy his network did not dissuade us from taking on the Iraqis in a war totally unrelated to 9/11.

Concern for pricing oil only in dollars helps explain our willingness to drop everything and teach Saddam Hussein a lesson for his defiance in demanding Euros for oil.

And once again there’s this urgent call for sanctions and threats of force against Iran at the precise time Iran is opening a new oil exchange with all transactions in Euros.

Using force to compel people to accept money without real value can only work in the short run. It ultimately leads to economic dislocation, both domestic and international, and always ends with a price to be paid.

The economic law that honest exchange demands only things of real value as currency cannot be repealed. The chaos that one day will ensue from our 35-year experiment with worldwide fiat money will require a return to money of real value. We will know that day is approaching when oil-producing countries demand gold, or its equivalent, for their oil rather than dollars or Euros. The sooner the better.

Saturday, February 25, 2006

Economic News

There are several MAJOR issues in the world today that are either adding to/or could add to our massive economic problems, and could eventually help tip the scales towards total economic catastrophe.

OIL

Yesterday a Suicide Attack on Saudi Arabia’s largest refinery caused Oil prices to jump $2.37 a barrel in one day of trading.

"It's new in the sense that this is the boldest attempt to strike at the heart of a Saudi oil- production complex," Antoine Halff, an oil analyst for Eurasia Group, said. "So far, they had been confined to office buildings and housing units."

Another article suggests this move "clearly signals that al-Qaeda is concentrating on oil, and not the government". Fimat analyst Mike Fitzpatrick said the Saudi incident added to jitters stemming from religious strife in Nigeria and concerns about Iraq and Iran. "Obviously, this has to heighten awareness of the increasing danger in that part of the world," he said.

Jim Lehrer NewsHour is reporting that Oil Supplies are Unstable and incorporates the perspectives of several smart folks.

VENEZUELA

In another move to create a rift between Hugo Chavez’s government and the US, Venezuela announced yesterday that it would prohibit Continental Airlines and Delta Air Lines from flying into their South American nation. They will also restrict flights by a third major U.S. carrier, American Airlines.

FANNIE MAE

Bloomberg is reporting that Fannie Mae Report Spotlights `Mind-Boggling' Accounting Errors.

``What do I have up my sleeve to solve an earnings shortfall?,'' Vice President of Financial Reporting Leanne Spencer asked Chief Financial Officer Timothy Howard.

The exchange was one of at least two deliberate attempts to fudge numbers to meet financial targets that led to $10.8 billion in accounting errors at the government-chartered company. The report concluded that Fannie Mae, which controlled assets exceeding $1 trillion, developed a culture that fostered misleading results and employed a staff ``unqualified'' to detect errors by top management.

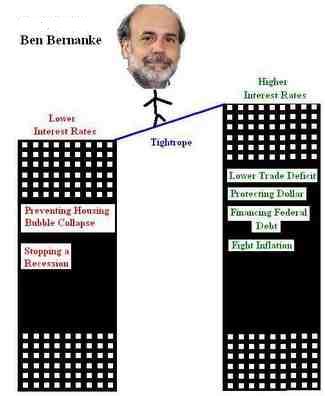

BERNANKE

According to this new Bloomberg report, the Helicopter man will continue with “Easy Al” Greenspan’s policy of not targeting asset bubbles, and will continue the policy of “mopping-up” after a burst.

Feb. 24 (Bloomberg) -- Federal Reserve Chairman Ben S. Bernanke, staking out a key policy in his first month on the job, said it's a ``bad idea'' for the central bank to try to influence housing and stock prices through interest-rate moves.

``To use interest rates to try to puncture the housing bubble would be a disastrously bad idea, and Bernanke obviously agrees, because he's not going to come close to doing that,'' said Alan Blinder, a former Fed vice chairman who is now a Princeton economics professor. He wrote a paper last year saying Greenspan might have been the ``greatest central banker'' ever.

Blinder said the Greenspan-Bernanke approach to bubbles is ``basically, you do nothing, and then the corollary to that is that you mop up after they burst to keep the financial system from taking a big fall.'' Bernanke's hands-off approach has ``been his position for years, since he was an academic,'' Blinder said.

GENERAL MOTORS

GM has more problems on the horizon. TheStreet.com reported yesterday: The Local 755 branch of the International Union of Electrical Workers-Communications Workers of America voted unanimously to authorize a strike if a bankruptcy judge cancels its labor contracts, according to a report from the Associated Press that cited Local 755 Chairman Keith Bailey. Local 755 represents 1,050 workers at a Delphi suspension parts plant in Kettering, Ohio, the A.P. said.

If Delphi workers go on strike, GM could end up in a standstill, and unable to get parts, they will bleed cash, increasing likelihood of ultimate Bankruptcy.

IRAQ

Sectarian violence continues to escalate in IRAQ. Reuters is reporting that Iraq is warning risk of endless civil war:

Iraq's defence minister warned of the risk of an endless "civil war" as sectarian violence flared again on Saturday, killing over 40, and Sunni and Shi'ite leaders met to try to halt four days of bloodshed.

With the gravest crisis since the U.S. invasion threatening his plan to withdraw 136,000 troops, U.S. President George W. Bush made a round of calls to Iraqi leaders on all sides urging them to work together to break a round of attacks sparked by the suspected al Qaeda bombing of a Shi'ite shrine on Wednesday.

"If there is a civil war in this country it will never end," Defence Minister Saadoun al-Dulaimi said earlier as a traffic ban around the capital was extended to Monday following attacks on Sunni mosques and car bomb in a Shi'ite holy city.

UAE PORT DEAL

Looks like the Bush Administration is taking a hard-line stance and won't reconsider the U.A.E. port deal. However, The Department of Homeland Security initially objected to the agreement.

ECONOMIC INDICATORS

INFLATION IS REARING ITS UGLY HEAD. Consumer Price Inflation is up .7% in January, as January Durables Orders Fell 10.2%. Also of Note: the Chinese YUAN hit new highs as the US dollar tumbled, and Gold soared $10 to close the week up 1%.

BIRD FLU

The Bird Flu is circling the globe like wildfire and has now made it to France and Germany. Experts are now saying “even if the current pandemic killing birds passes, no one should breathe a sign of relief because the threat to people will not be gone.”

"At best, a containment policy will only postpone the emergence of a pandemic, 'buying time' to prepare for its effects," Dr Marc Lipsitch and colleagues from the Harvard School of Public Health and Dr Carl Bergstrom from the University of Washington wrote.

IRAN-USA

This article is well worth the time spent reading it, and states that (based on their research and analysis), our current situation with IRAN could turn into a complete financial crisis of a scope comparable with that of 1929.

IMHO, based on trends & analysis of current information, I honestly believe our country and economy are headed towards very tough times.

OIL

Yesterday a Suicide Attack on Saudi Arabia’s largest refinery caused Oil prices to jump $2.37 a barrel in one day of trading.

"It's new in the sense that this is the boldest attempt to strike at the heart of a Saudi oil- production complex," Antoine Halff, an oil analyst for Eurasia Group, said. "So far, they had been confined to office buildings and housing units."

Another article suggests this move "clearly signals that al-Qaeda is concentrating on oil, and not the government". Fimat analyst Mike Fitzpatrick said the Saudi incident added to jitters stemming from religious strife in Nigeria and concerns about Iraq and Iran. "Obviously, this has to heighten awareness of the increasing danger in that part of the world," he said.

Jim Lehrer NewsHour is reporting that Oil Supplies are Unstable and incorporates the perspectives of several smart folks.

VENEZUELA

In another move to create a rift between Hugo Chavez’s government and the US, Venezuela announced yesterday that it would prohibit Continental Airlines and Delta Air Lines from flying into their South American nation. They will also restrict flights by a third major U.S. carrier, American Airlines.

FANNIE MAE

Bloomberg is reporting that Fannie Mae Report Spotlights `Mind-Boggling' Accounting Errors.

``What do I have up my sleeve to solve an earnings shortfall?,'' Vice President of Financial Reporting Leanne Spencer asked Chief Financial Officer Timothy Howard.

The exchange was one of at least two deliberate attempts to fudge numbers to meet financial targets that led to $10.8 billion in accounting errors at the government-chartered company. The report concluded that Fannie Mae, which controlled assets exceeding $1 trillion, developed a culture that fostered misleading results and employed a staff ``unqualified'' to detect errors by top management.

BERNANKE

According to this new Bloomberg report, the Helicopter man will continue with “Easy Al” Greenspan’s policy of not targeting asset bubbles, and will continue the policy of “mopping-up” after a burst.

Feb. 24 (Bloomberg) -- Federal Reserve Chairman Ben S. Bernanke, staking out a key policy in his first month on the job, said it's a ``bad idea'' for the central bank to try to influence housing and stock prices through interest-rate moves.

``To use interest rates to try to puncture the housing bubble would be a disastrously bad idea, and Bernanke obviously agrees, because he's not going to come close to doing that,'' said Alan Blinder, a former Fed vice chairman who is now a Princeton economics professor. He wrote a paper last year saying Greenspan might have been the ``greatest central banker'' ever.

Blinder said the Greenspan-Bernanke approach to bubbles is ``basically, you do nothing, and then the corollary to that is that you mop up after they burst to keep the financial system from taking a big fall.'' Bernanke's hands-off approach has ``been his position for years, since he was an academic,'' Blinder said.

GENERAL MOTORS

GM has more problems on the horizon. TheStreet.com reported yesterday: The Local 755 branch of the International Union of Electrical Workers-Communications Workers of America voted unanimously to authorize a strike if a bankruptcy judge cancels its labor contracts, according to a report from the Associated Press that cited Local 755 Chairman Keith Bailey. Local 755 represents 1,050 workers at a Delphi suspension parts plant in Kettering, Ohio, the A.P. said.

If Delphi workers go on strike, GM could end up in a standstill, and unable to get parts, they will bleed cash, increasing likelihood of ultimate Bankruptcy.

IRAQ

Sectarian violence continues to escalate in IRAQ. Reuters is reporting that Iraq is warning risk of endless civil war:

Iraq's defence minister warned of the risk of an endless "civil war" as sectarian violence flared again on Saturday, killing over 40, and Sunni and Shi'ite leaders met to try to halt four days of bloodshed.

With the gravest crisis since the U.S. invasion threatening his plan to withdraw 136,000 troops, U.S. President George W. Bush made a round of calls to Iraqi leaders on all sides urging them to work together to break a round of attacks sparked by the suspected al Qaeda bombing of a Shi'ite shrine on Wednesday.

"If there is a civil war in this country it will never end," Defence Minister Saadoun al-Dulaimi said earlier as a traffic ban around the capital was extended to Monday following attacks on Sunni mosques and car bomb in a Shi'ite holy city.

UAE PORT DEAL

Looks like the Bush Administration is taking a hard-line stance and won't reconsider the U.A.E. port deal. However, The Department of Homeland Security initially objected to the agreement.

ECONOMIC INDICATORS

INFLATION IS REARING ITS UGLY HEAD. Consumer Price Inflation is up .7% in January, as January Durables Orders Fell 10.2%. Also of Note: the Chinese YUAN hit new highs as the US dollar tumbled, and Gold soared $10 to close the week up 1%.

BIRD FLU

The Bird Flu is circling the globe like wildfire and has now made it to France and Germany. Experts are now saying “even if the current pandemic killing birds passes, no one should breathe a sign of relief because the threat to people will not be gone.”

"At best, a containment policy will only postpone the emergence of a pandemic, 'buying time' to prepare for its effects," Dr Marc Lipsitch and colleagues from the Harvard School of Public Health and Dr Carl Bergstrom from the University of Washington wrote.

IRAN-USA

This article is well worth the time spent reading it, and states that (based on their research and analysis), our current situation with IRAN could turn into a complete financial crisis of a scope comparable with that of 1929.

IMHO, based on trends & analysis of current information, I honestly believe our country and economy are headed towards very tough times.

Wednesday, February 22, 2006

Commercial Real Estate Bubble?

Today, I had to investigate why my Blog was receiving more hits than usual. After examining the issue, I quickly came to the realization that my site was mentioned in a BusinessWeek blurb concerning Real Estate, and people were curiously checking in.

Anyway, a hearty “thank you” to BusinessWeek for the plug, but I must admit that my feelings go against the general thoughts/comments in the article linking to me—“No Commercial Real Estate Bubble.”

Those who have taken the time to read my Blog will quickly understand that my philosophy takes into account numerous factors, and I feel the U.S. housing bubble is only the latest (albeit huge) symptom of much larger fundamental economic imbalances that will soon start to correct.

My belief is: Our U.S. Housing Bubble is the direct result of massive Fed liquidity, several years of ultra-low interest rates, relaxed lending standards, high use of non-conventional mortgages, general economic euphoria and irrational exuberance on the part of realtors, loan agents, speculators, new homeowners and the general public.

I also feel it was part of Alan Greenspan’s “Master Plan” to create a new asset bubble in an effort to help the U.S. get out of a recessionary period (post stock market crash and 9/11). In his endeavor to stimulate the economy, Mr. Greenspan swiftly opened the money spigots, and dropped interest rates to a 40-year low. Alan then blew more oxygen into the bubble by recommending the use of adjustable & non-conventional mortgages…the bubble grew.

Ultimately his plan worked, as housing prices rose, consumers spent like crazy (using their homes as ATM’s), construction permits soared, U.S. GDP grew, the Stock market re-inflated, and here we are today… dumb, fat, happy and completely oblivious to the huge economic problems at our doorstep.

If we take a casual look at our country’s economic situation today, everything looks real good on the surface, but strip back a couple of layers and things get real ugly, real quick:

- Our trade deficit is at an all time high—again! ($726B)

- Cumulative government debt is soaring ($8.25T)

- We have exceeded our congressionally authorized debt ceiling ($8.184T)

- Massive fed liquidity; M3 is greater than $10 Trillion dollars

- Foreign Central Banks own ~ $3 Trillion U.S. Debt

- Foreigners could dump their dollars/wreck our economy at will

- We Americans consume ~ 80% of world’s savings to maintain our lifestyle

- U.S. has massively outsourced blue/white collar jobs--continues to do so

- Consumer spending/housing were responsible for 90% of growth in GDP

- U.S. savings rates are negative--not seen since the great depression

- New day of increasing interest rates—possibly higher than predicted

- Lending practices will soon start to tighten up as risks increase

- Inflation is rising—probably much higher than gvt’s manipulated figures

- Housing market cooling--taking away consumer wealth effect/housing ATM

- Interest rates will reset on > $1 Trillion in mortgages in next 18 months

- Inverted Yield curve (possible recession on the horizon?)

- GM, FORD, DELPHI, US Airlines and many others are struggling

- Oil is currently a major issue (world supply/demand and higher prices)

- Numerous issues w/ IRAN, Venezuela and Nigeria

- Oil could rise to > $100 barrel this year and clobber the world economy

Anyway, a hearty “thank you” to BusinessWeek for the plug, but I must admit that my feelings go against the general thoughts/comments in the article linking to me—“No Commercial Real Estate Bubble.”

Those who have taken the time to read my Blog will quickly understand that my philosophy takes into account numerous factors, and I feel the U.S. housing bubble is only the latest (albeit huge) symptom of much larger fundamental economic imbalances that will soon start to correct.

My belief is: Our U.S. Housing Bubble is the direct result of massive Fed liquidity, several years of ultra-low interest rates, relaxed lending standards, high use of non-conventional mortgages, general economic euphoria and irrational exuberance on the part of realtors, loan agents, speculators, new homeowners and the general public.

I also feel it was part of Alan Greenspan’s “Master Plan” to create a new asset bubble in an effort to help the U.S. get out of a recessionary period (post stock market crash and 9/11). In his endeavor to stimulate the economy, Mr. Greenspan swiftly opened the money spigots, and dropped interest rates to a 40-year low. Alan then blew more oxygen into the bubble by recommending the use of adjustable & non-conventional mortgages…the bubble grew.

Ultimately his plan worked, as housing prices rose, consumers spent like crazy (using their homes as ATM’s), construction permits soared, U.S. GDP grew, the Stock market re-inflated, and here we are today… dumb, fat, happy and completely oblivious to the huge economic problems at our doorstep.

If we take a casual look at our country’s economic situation today, everything looks real good on the surface, but strip back a couple of layers and things get real ugly, real quick:

- Our trade deficit is at an all time high—again! ($726B)

- Cumulative government debt is soaring ($8.25T)

- We have exceeded our congressionally authorized debt ceiling ($8.184T)

- Massive fed liquidity; M3 is greater than $10 Trillion dollars

- Foreign Central Banks own ~ $3 Trillion U.S. Debt

- Foreigners could dump their dollars/wreck our economy at will

- We Americans consume ~ 80% of world’s savings to maintain our lifestyle

- U.S. has massively outsourced blue/white collar jobs--continues to do so

- Consumer spending/housing were responsible for 90% of growth in GDP

- U.S. savings rates are negative--not seen since the great depression

- New day of increasing interest rates—possibly higher than predicted

- Lending practices will soon start to tighten up as risks increase

- Inflation is rising—probably much higher than gvt’s manipulated figures

- Housing market cooling--taking away consumer wealth effect/housing ATM

- Interest rates will reset on > $1 Trillion in mortgages in next 18 months

- Inverted Yield curve (possible recession on the horizon?)

- GM, FORD, DELPHI, US Airlines and many others are struggling