Many economic optimists feel that yesterday’s report on January’s record number of housing starts was dirt kicked in the face of Housing Bubble theorists. I completely disagree with that position, and believe the news only exacerbates the coming Bubble collapse.

Recently, Toll Brothers CEO, Robert Toll, said that speculators are canceling their contracts and exiting the market, while prospective buyers, sensing a slowdown, are no longer eager to commit to homes with a long delivery lag time.

With the increasing number of canceled home orders, and a drop of new-home sales (as reported by KB, Toll Brothers, Ryland, and Standard Pacific home builders) what will happen to all these new homes once they are actually built and on the market? Answer: They will add to the already increasing inventories, and with increasing mortgage rates, fewer speculators and a cooling housing market, these homes will have a very difficult time finding new owners.

We are already starting to see builders engage in heavy discounting and promotional activity. According to Capuchinomics, a recent National Association of Homebuilders survey found that 64% of builders are offering incentives like free upgrades and/or reduced/zero closing costs; and 19% are cutting prices.

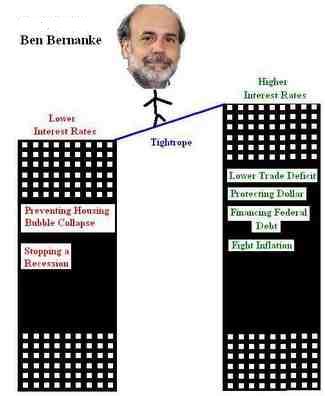

With all this said, recent congressional comments from Big Money Ben Bernanke (BMBB) suggest that he may raise rates well beyond what many had previously forecasted (1 more hike w/stop at 4.75%). This new info is certainly great news for the US dollar--which is the real “unspoken” reason for higher rates, but it’s terrible for the housing sector, as any further increase beyond the already assumed 4.75% stopping point will drive mortgage rates even higher, will further invert the yield curve (a telltale sign of looming recession), and will clobber roughly 7 million homeowners (holding > $1 Trillion in mortgages) when their interest-only ARM’s reset in the coming 12-18 months.

Add the issues above to the numerous other concerns that I have previously pointed out, (negative personal savings rates--not seen since the Great Depression, home delinquency notice increases, increases in credit card delinquencies, record bankruptcies, potential oil supply concerns, higher energy prices, higher inflation than that reported, completely oblivious consumers displaying irrational exuberance, etc), and I think we have a catastrophe waiting to happen.

Time will only tell, but I’m definitely not optimistic about the report.

What are your thoughts on the subject?

9 comments:

As I read real estate pundits, they hedge, (maybe a slow down, maybe a soft landing, maybe flat prices, and maybe a stall).

Well if an airplane stalls it crashes. So will be the Real Estate Crash and Burn. There are no homes a college graduate can buy. The real Inflation including homes is outrageous.

I looked at an open house in Los Angeles Sunday. I simply asked the real estate lady what she thought about the real estate bubble. She said, "There is no Bubble". Then she immediately turned and walked away. So there you have it. "NO BUBBLE"

That is absolutely hilarious!

Another completely oblivious, irrationally exuberant realtor. Hope she has another line of work available...

I'm debating how to manage my retirement savings. I'm only 6 years out of college and I've managed to do well.

Last year I had my money in emerging markets (foreign companies can compete with cheap labor), s&p (earnings-per-share are pretty good) and gold (obvious). I did well.

This year, as we potential enter a downturn in the economy, I'm debating what percentage of my retirement I should put into short term bonds.

devil's advocate says that a catastrophe has been predicted ever since the stock market crash of '87. Back then it was Japan's lending to US that would stall, then it was the housing crash of the 1990's, then it was emerging markets, then the tech crash...

I think a serious slowdown in the US is very likely, because in all of those past examples, the Fed had the power to inject liquidity by lowering rates but it doesn't have the luxury today.

Question then, is whether US goes for inflation or a massive contraction in demand. it takes a hell of a lot of chutzpah for a politician (and the Fed are politicos) to sit back and talk about the value of low inflation when house values are down 50%, uneployment is up and the poor sucker that borrowed 5x the old salary to own a crappy house in a sketchy neighbourhood is now paying off a mortgage on a house that is worth half, or less than the purchase price.

More likely that they'll just keep printing the cash, I think

Anonymous,

Another variable you neglected to consider is: foreign support & demand for the USD.

The Fed is currently raising rates under the stated position of keeping inflation at bay. I believe “inflation” is only part of the equation, and the real (unstated) reason behind the increases is to garner further support for the Dollar.

I agree we’ll continue to see massive liquidity, but in the same breath, the Fed will need to keep higher rates in order to stave off a serious devaluation of the USD. If the dollar does fall in value, we will then see massive inflation as everything we import become more expensive.

From my perspective the Fed has 2 choices:

(1) Save the US housing market

(2) Save the US Dollar

I believe he’ll try to accomplish both, but don’t believe for a moment that he’s going to be successful

Something to ponder at the Office of Federal Housing Enterprise oversight. House price appreciation continues at a robust pace. So much for a "bubble".

http://www.ofheo.gov/media/pdf/4q05hpi.pdf

The housing bubble was sort of like a run away train.

Please add good good information that would help others in such best way.This post is exactly what I am concerned. we need some more reliable information.

Their is no budget.

Post a Comment